%20(2).png)

Is Trophic Coherence a Structural Source of Economic and Financial Stability?

- Feb 1, 2021

- 5 min read

Nicholas Beale, Richard Gunton, Sam Johnson, Marcus Miller, Bazil Sansom, Robert MacKay

Two things we think are crystal clear

Especially after this strange year

The first: it is indeed a fable

To think economies are stable.

Second: Thinking of ecology

Is critical to the economy

Of the specific things we’ve learned:

By using some neat maths, we’ve turned

The trophic incoherence notion

(Which works with fishes in the ocean)

Into a thing with some ability

To offer insight on stability

The wider message seems to be

Systems you cannot touch or see

Can be important and are there

So study them, and be aware

In our project for Rebuilding Macroeconomics, we explore whether trophic coherence may be a structural source of stability in economic and financial networks.

What, you may ask, is trophic coherence and why does it matter?

Fig.1: An example of a perfectly coherent network.

Trophic coherence quantifies the extent to which the nodes of a directed network can be assigned levels so that the change of level along each edge is +1 (Fig.1 illustrates a perfectly coherent network). The coherence of a network is reduced by the presence of cycles (feed-back) and of feed-forward structure in the network (see Fig.2) and can be thought of as measuring the directionality of a network (explained in our previous blog post).

Trophic coherence is a concept introduced by our team member Sam Johnson with the original goal of explaining why ecological food webs – the interconnected and overlapping food chains in an ecosystem - are relatively stable despite arguments that typical large complex systems should be

unstable.

We ask whether trophic coherence may also be a structural source of stability in complex economic and financial systems.

Fig.2: simple feed-back loop (FBL) and feed-forward loop (FFL) motifs. The presence of feed-back and feed-forward structure reduces the trophic coherence of a network.

The original definition of trophic coherence requires nodes in the network with no incoming links – ‘basal nodes’. However many key economic and financial networks may not have any basal nodes at all. We therefore started by introducing an improved method that overcomes this methodological limitation (published here) opening the way for a new programme of work for economics and finance.

Armed with this new tool, we make an initial exploration of the relevance of trophic structure for macro relevant dynamics in two paradigmatic economic and financial systems: in interbank funding networks; and production networks. We find evidence that trophic incoherence drives systemic risk in financial exposure networks; and that sectoral employment cycle co-movement is positively correlated with trophic incoherence (suggesting it may be relevant for understanding business cycle dynamics).

These results suggest trophic structure may be relevant for dynamics in a broad range of economic systems, meriting further research.

Trophic incoherence drives systemic risk in financial exposure networks.

A key response following the Global Financial Crisis (GFC) of 2007-8 has been to increase required capital buffers, and introduce regulatory liquidity buffers to increase the resilience of banks to adverse shocks.

However one important lesson of the financial crisis was that we learnt the system can collapse even if, individually, institution by institution both solvency and liquidity positions seem quite safe.

Speaking for Rebuilding Macroeconomics earlier this year, Alex Brazier (Executive Director for Financial Stability at the Bank of England) states:

“…it’s not about measuring the value at risk of an individual balance sheet - which may be very low - it’s about measuring the knock on effects and simulating the knock on effects, through the system, of something that looks individually very safe.” (Full speech here).

However the magnitude of this sort of network-based amplification of distress, and how easily distress can propagate in the system, may be deeply dependent on the pattern of connections among financial institutions. We investigate how trophic structure of an interbank network influences financial contagion dynamics (see our Rebuilding Macro working paper).

Following the financial contagion literature we construct simulated banking systems that are composed of a number of banks connected by interbank lending/borrowing relationships (illustrated in Fig.3). We simulate networks with the same number of banks, links and total interbank lending, but varying levels of trophic coherence, and varying levels of balance sheet leverage.

We use DebtRank to measure the response of the system to an exogenous shock to the value of banks’ assets (DebtRank is a benchmark model of financial contagion[1] introduced by Stefano Battiston and co-authors and now widely employed in systemic risk analysis and monitoring).

We find that the trophic structure of the interbank network has a crucial influence on the dynamics: endogenous shock-amplification is systematically higher in more incoherent networks, even when banks have large capital buffers making them appear extremely safe (See Fig.4).

Fig.4: Total system level losses (measured as total relative equityloss using DebtRank) in response to a uniform shock to bank assets, vs. trophic incoherence (x-axis) and balance sheet leverage (y-axis).

These results imply that buffers alone may not necessarily be enough, but also that in principle, systemic risk could be significantly reduced without increasing costly capital requirements, ‘simply’ by re-wiring the exposure network to achieve a more coherent pattern of exposures.

We propose that e.g. an additional (transaction level) regulatory capital requirement or tax that is proportional to the trophic level difference from 1 between counterparties (and zero for a level difference of 1), would encourage the self-organised formation of a more coherent network structure, reducing systemic risk without reducing the value of interbank lending, or the need to increase regulatory capital.

Sectoral employment cycle co-movement is related to trophic incoherence

The defining feature of business cycles is the comovement of production and employment across the different sectors of the economy. Most of modern macroeconomics has assumed this comovement is driven by aggregate shocks of some sort or other, while sector specific shocks are believed to average out (as argued in Lucas’s (1977) famous essay on business cycles).

There is growing interest however, in whether comovement between sectors may be the endogenous outcome of sector specific shocks propagating across production networks in which sectors both buy from and sell to each other.

In particular it has been argued that shocks hitting sectors that are particularly important as suppliers to other sectors (‘hub’ sectors in the network) will not wash out and can translate into aggregate fluctuations (see in particular the work of Daron Acemoglu and of Vasco Carvalho).

We investigate whether the trophic incoherence of intermediate production structures may influence sectoral comovement - thus aggregate business cycle fluctuations.

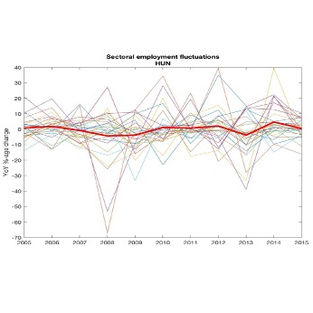

Fig.5: Examples of fluctuations in sectoral employment (Hungary – LHS, and Spain - RHS).

We find that this holds in the data: we exploit cross-sectional variation across national economies. We find that the average correlation of employment fluctuations across sectors is higher for national economies with more incoherent domestic production network structures (and vice versa) (see Fig.6) – although interestingly the U.S. is a significant outlier.

This is consistent with the possibility that the network of input-output relationships play a role in propagating shocks between sectors, mediated by trophic structure of the network. This may be relevant not only for understanding national business cycles, but e.g. also suggest a potential link between the changing structure of global supply chains, and international business cycle co-movement.

Fig.6: sectoral employment cycle co-movement vs. production network incoherence.

Our results suggest trophic structure may be relevant for dynamics in a broad range of economic systems, meriting further research.

These results are only a first step in exploring whether trophic coherence may be a structural source of stability in economic and financial networks. They suggest trophic coherence may be a structural property with important implications for a broad range of economic systems and macro-relevant problems in economics. Moreover, they also suggest that the link between trophic structure and (in)stability could potentially offer new strategies for managing the resilience of e.g. financial, production and trade networks. We see a wide range of opportunities for future research exploring the meaning and influence of trophic structure in different systems, and on different sorts of dynamics and transmission mechanisms.

Footnotes:

[1] DebtRank models the following contagion process: if a bank suffers an equity loss, its probability of default will increase. Its counterparties will account for this increased default risk by reducing the value of the interbank asset on their balance sheet, which – since what they owe to their creditors and depositors has not changed - reduces their equity by the same amount. The process of re-evaluation of interbank assets and equities thus propagates across the interbank network.

Comments